FBR has prioritized establishment of a Compliance Risk Management (CRM) Directorate as a key area for Domestic Revenue Mobilization. The necessary legal requirement for establishment of Directorate General Compliance Risk Management was met in Finance Act, 2021, whereby, an amendment was introduced vide Section 230I of Income Tax Ordinance, 2001 for establishment of Directorate General of Compliance Risk Management. Accordingly, FBR established a Compliance Risk Management Directorate in Inland Revenue Service on 07th November, 2022 as a step forward in identification, assessment and prioritization of compliance risks. CRM is based on risk management and backed by organizations like the OECD. It is a systematic approach in identifying, assessing, ranking, and addressing tax compliance risks based on diverse data sources. This enhances decision-making and adherence to tax laws.

CRM promotes voluntary tax compliance by identifying risks, executing audits, and enhancing revenue through taxpayer segmentation. It includes targeted campaigns, and behavioral change efforts to address noncompliance, with feedback mechanisms ensuring responsiveness to taxpayer concerns. CRM uses AI/ML techniques to address issues of non-filing, under-filing and tax evasion.

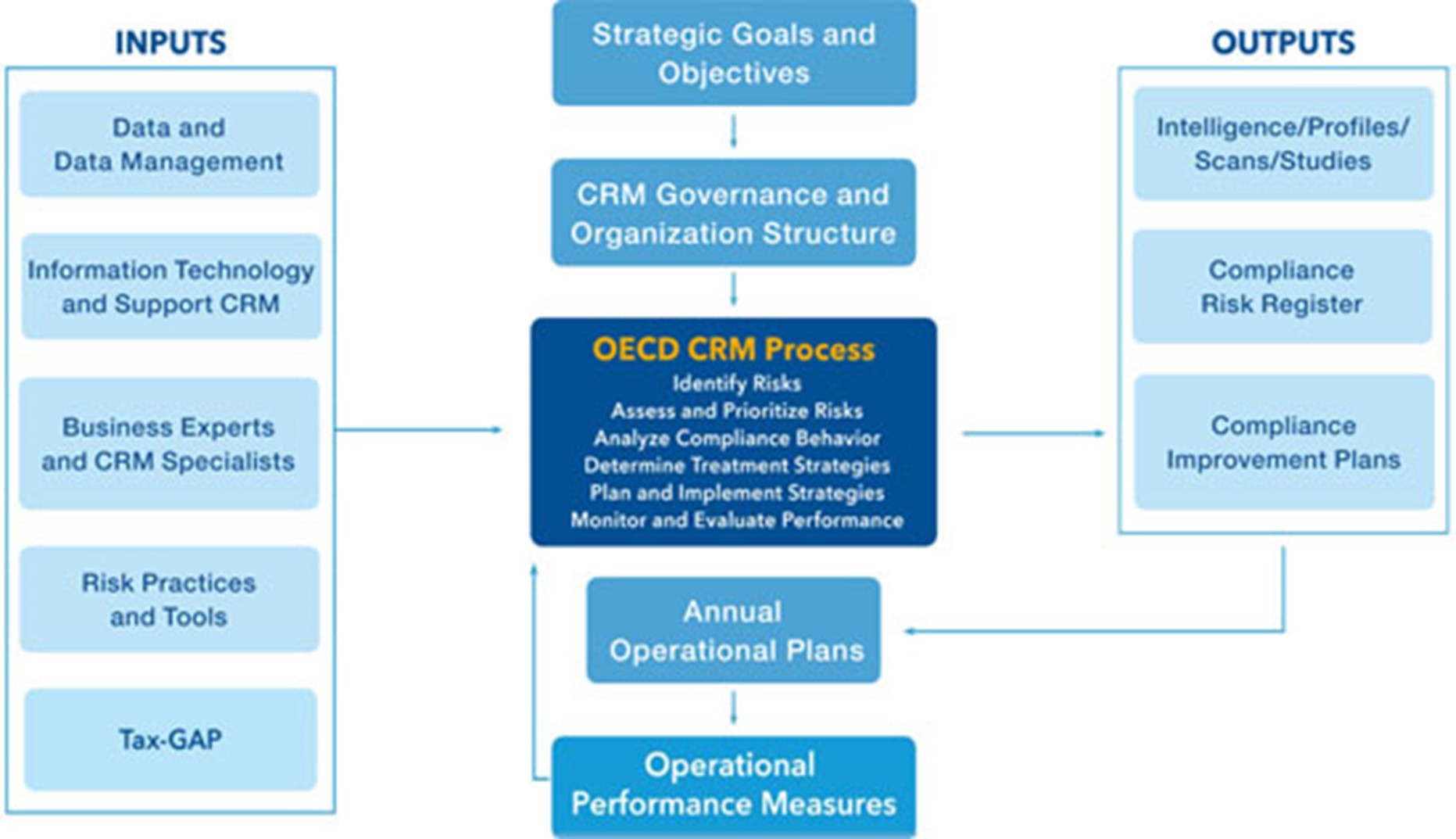

Organisation for Economic Co-operation and Development (OECD) places the CRM process within a broader framework that includes the key inputs, outputs, and other CRM prerequisites.

CRM (Compliance Risk Management) and traditional tax audits differ in several key areas.

CRM is proactive, addressing compliance risks through behaviour analysis, while traditional audits are reactive, focusing on specific taxpayer records after filing.

CRM includes risk assessment, segmentation, education, and outreach to enhance compliance, whereas traditional audits verify the accuracy of individual financial records.

CRM utilizes data analytics and third-party information to prioritize compliance efforts, while traditional audits depend largely on taxpayer-provided documents and offer less analytical depth.

CRM encourages voluntary compliance, reduces the tax gap, and fosters trust through education. In contrast, traditional audits identify noncompliance, impose penalties, and recover unpaid taxes.

CRM promotes collaboration within tax authorities, while traditional audits often create a punitive and adversarial atmosphere.

Data and analytics enhance CRM effectiveness. Key aspects include:

| Risk Detection: Modern CRM' utilize data to analyze large datasets, identifying risk clusters among taxpayer segments and prioritizing risks contributing to the tax gap. |

| Third-Party Data: Accessing external information supports risk detection and improves tax collections by identifying instances of noncompliance. |

|

Targeted Campaigns: Data analytics foster targeted compliance efforts in low-adherence sectors, enhancing trust in the tax system. |

|

Automation: Machine Learning (ML) based systems facilitating data sharing are essential for effective CRM, streamlining processes, and managing compliance risks systematically. |

CRM dashboards have recently been deployed in the Field Formations as a decision support system. The dashboard helps to conduct desk audit of high-risk cases, whereas the follow-up action has to be proceeded with as per law.